Title insurance in Florida protects one of the most important parts of a real estate purchase: your right to own the property after closing.

Most buyers spend a lot of time looking at price, location, rental income, HOA fees, mortgage terms, and property condition. Those details matter. But if the title has a hidden problem, even a beautiful Miami condo or South Florida investment property can turn into a stressful and expensive mistake.

This is especially important for Canadian buyers, snowbirds, and long-distance investors who may not be familiar with Florida closing customs. You may be buying from Toronto, Montreal, Vancouver, Calgary, or elsewhere in Canada, while the property, title company, closing agent, lender, seller, HOA, and county records are all in Florida.

The goal of this guide is simple: to explain title insurance in Florida in plain language, show what buyers should review before closing, and help you understand where title protection fits into the larger Miami and South Florida due diligence process.

Why Title Insurance in Florida Matters More Than Buyers Expect

When you buy real estate, you are not only buying walls, floors, views, parking spaces, or rental potential. You are buying legal ownership.

That ownership history may include previous mortgages, contractor liens, unpaid taxes, association claims, estate issues, divorce judgments, recording errors, easements, old deeds, or other problems that are not obvious during a showing.

Title insurance in Florida is designed to help protect against covered title issues connected to the property’s ownership history. Without it, a buyer may have to deal with a title claim personally after closing.

For a local buyer, that is already inconvenient. For a Canadian buyer or international investor managing a property from another country, it can be even more complicated. You may need legal help, local representation, document review, wire coordination, tax advice, and property management support all at once.

That is why title review should not be treated as a last-minute closing detail. It belongs in the same conversation as financing, inspections, HOA documents, insurance, taxes, and long-term ownership planning.

What Title Insurance in Florida Actually Protects

Title insurance in Florida is different from homeowners insurance or condo insurance.

Homeowners insurance usually protects against future property damage, depending on the policy. Title insurance is focused on ownership risks tied to the past. It looks backward at the chain of ownership and helps protect against certain covered problems that existed before you became the owner.

Common title issues can include unpaid liens, incorrect legal descriptions, forged signatures, missing heirs, improperly recorded documents, unresolved mortgages, judgments, tax claims, boundary issues, or mistakes in public records.

Before closing, the title company or closing agent usually performs a title search through public records. In Miami-Dade, buyers and advisors may also review information through the Miami-Dade Clerk Official Records system as part of early research.

That does not replace professional title work, but it helps buyers understand why ownership history matters.

A simple question buyers often ask is: “If the title company already searches the records, why do I still need title insurance?”

The answer is that a title search reduces risk, but it does not eliminate every possible hidden issue. Title insurance in Florida provides a layer of protection after closing if a covered title problem later appears.

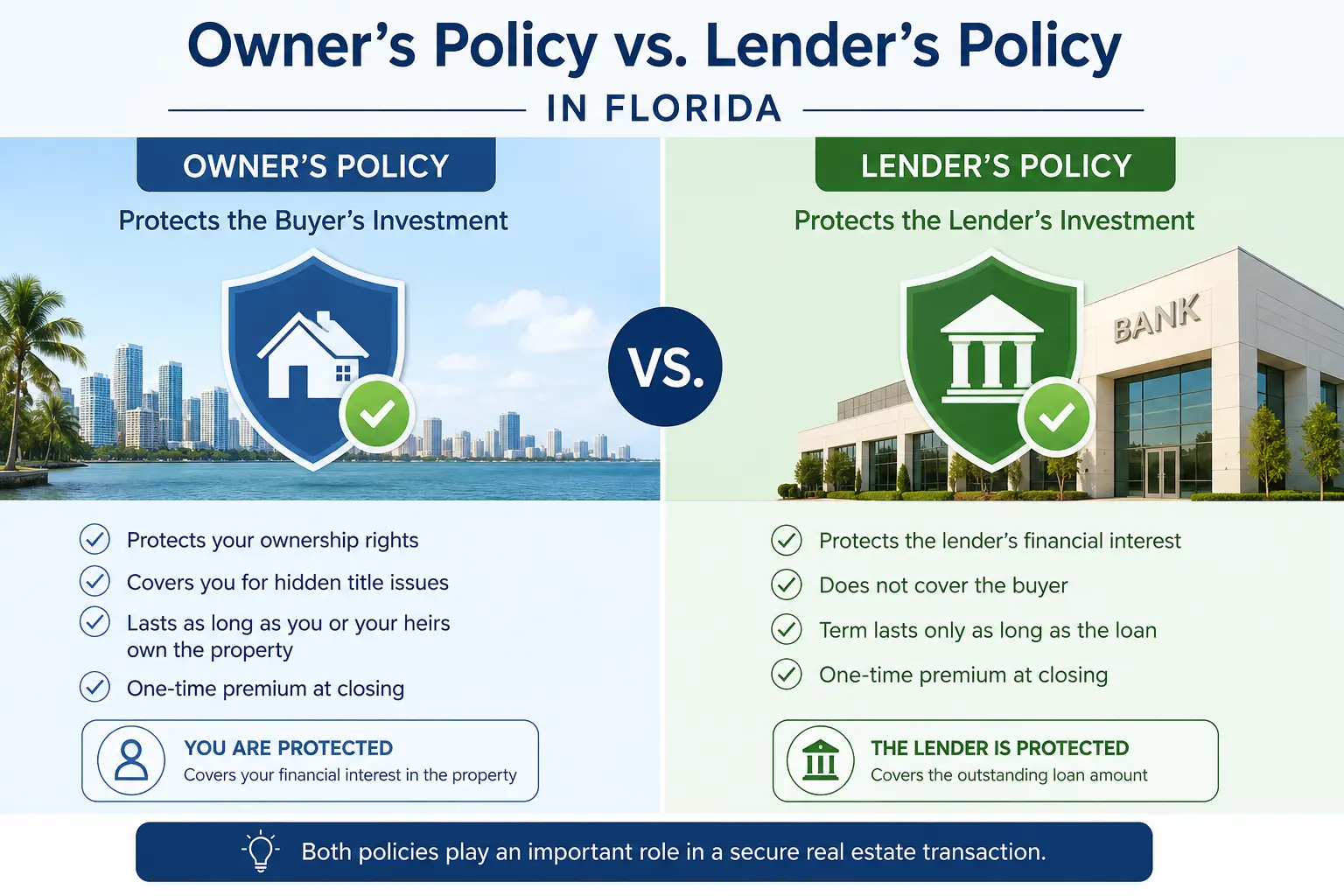

Owner’s Policy vs. Lender’s Policy: Know the Difference

One of the biggest misunderstandings about title insurance in Florida is the difference between an owner’s policy and a lender’s policy.

If you are financing the purchase, your lender will usually require a lender’s title insurance policy. That policy protects the lender’s interest in the property, not your personal equity as the buyer.

An owner’s title insurance policy is the policy that protects the buyer’s ownership interest, subject to the policy terms, exceptions, and exclusions.

| Policy Type | Who It Protects | When It Matters | Buyer Takeaway |

|---|---|---|---|

| Owner’s title policy | The property buyer | If a covered ownership issue appears after closing | Important for protecting your equity and ownership rights |

| Lender’s title policy | The mortgage lender | If a covered title issue affects the lender’s security interest | Usually required when financing, but it does not protect the buyer’s equity |

Cash buyers sometimes ask, “Do I still need owner’s title insurance if I do not have a mortgage?”

In many cases, the answer is yes. Paying cash removes the lender from the transaction, but it does not remove title risk. If anything, cash buyers should be especially careful because their own funds are fully exposed.

For Canadian buyers paying cash from Canada, title insurance in Florida can be an important part of protecting a large cross-border capital transfer.

7 Powerful Checks Before You Rely on Title Insurance in Florida

Title insurance is important, but buyers should not use it as an excuse to skip due diligence. The smarter approach is to review the property carefully before closing and use the title process as one part of a larger risk-management plan.

1. Confirm Who Is Paying for the Owner’s Policy

Who pays for title insurance in Florida can depend on the county, local custom, contract terms, and negotiation.

In parts of South Florida, buyers may commonly pay for the owner’s title policy, while other counties may follow different customs. The important point is not to assume. Ask early, confirm the contract language, and understand whether the title and closing costs are built into your budget.

If you are comparing properties in Miami, Fort Lauderdale, Boca Raton, or West Palm Beach, the closing cost structure may not look identical in every transaction. Buyers should review this with their real estate advisor, closing agent, and legal support before the inspection period ends.

For a broader ownership budget, compare title costs alongside Florida property taxes for non-residents, Miami property insurance costs, HOA fees, financing costs, and property management expenses.

2. Review the Title Commitment Carefully

The title commitment is not just paperwork. It is a preview of what the title insurer is willing to insure, what must be cleared before closing, and what exceptions may remain after closing.

Buyers should pay attention to liens, mortgages, easements, restrictions, judgments, unpaid taxes, open permits, association claims, and any unusual exceptions.

If something is unclear, ask questions. Do not wait until the day before closing.

This is where a trusted closing team matters. Miami P&B Investments’ real estate legal services in Miami can help buyers coordinate the right professional review when title questions, contract concerns, or ownership-structure issues need deeper attention.

3. Match the Legal Description to the Property

A property address is not the same as the legal description.

The legal description identifies exactly what is being transferred. For condos, it may reference the unit, building, condominium declaration, assigned parking, storage, or other recorded details. For single-family homes, it may involve lot, block, subdivision, and recorded plat information.

Before closing, buyers should make sure the legal description aligns with what they believe they are buying.

This is especially important in Miami and South Florida, where buyers may be comparing waterfront homes, condo units, townhomes, investment properties, and mixed-use opportunities. A mistake in the legal description can create confusion later.

4. Check for Liens, Judgments, and Unpaid Association Balances

Title insurance in Florida often intersects with liens and unpaid obligations.

A seller may have an outstanding mortgage that must be paid off at closing. A contractor may have filed a lien for unpaid work. A condo or HOA may claim unpaid assessments, late fees, violations, or transfer charges. Taxes may need to be prorated or paid. Court judgments can also create problems.

For condo buyers, this is where title review overlaps with association due diligence. You should not only review title documents. You should also review condo budgets, reserves, meeting minutes, insurance, special assessments, rental rules, and estoppel information.

Miami P&B Investments has separate buyer guides on Florida condo documents, Florida condo milestone inspections, and non-warrantable condos in Florida. Those topics connect closely to title and closing risk, even though they are not the same thing.

5. Understand Documentary Stamps and Recording Costs

Florida closings can include documentary stamp taxes, recording charges, title search fees, closing fees, lender charges, and other transaction costs.

The Florida Department of Revenue documentary stamp tax page is a helpful external reference for understanding why certain recorded real estate documents may trigger documentary stamp taxes.

For buyers, the practical point is simple: do not review the title policy in isolation. Review the full closing statement.

Canadian buyers should also convert U.S. dollar closing costs into Canadian dollars when planning total cash needed. A cost that looks modest in USD can become more meaningful after exchange-rate movement, wire fees, and timing differences.

For a deeper cross-border view, read Miami P&B Investments’ guide on managing currency exchange risk when buying in Miami.

6. Ask How Title Insurance in Florida Fits Your Financing Plan

If you are using a mortgage, your lender will have title requirements. The lender may require a lender’s policy, specific endorsements, closing instructions, wire procedures, and timing rules.

For Canadian buyers, financing can involve additional documentation, larger down payments, foreign credit review, income verification, reserve requirements, and cross-border banking coordination.

That means title insurance in Florida should be reviewed alongside your loan approval timeline.

If the lender needs a title issue cleared before funding, it can affect closing. If a title exception is unacceptable to the lender, the deal may need to be corrected, renegotiated, or delayed.

Buyers exploring financing should review the Miami P&B Investments guide on U.S. mortgages for Canadians in Florida before finalizing a closing timeline.

7. Make Sure Your Ownership Structure Is Clear

How you take title matters.

Will the property be owned individually, jointly with a spouse, through an LLC, through a corporation, through a trust, or another structure? The right answer depends on your goals, tax situation, estate planning needs, liability concerns, financing, and rental strategy.

This is not a decision to make casually at the closing table.

For Canadian investors, ownership structure can affect U.S. tax reporting, Canadian reporting, liability planning, financing, estate considerations, and future sale strategy. Before choosing a structure, speak with qualified legal and tax professionals who understand cross-border real estate ownership.

Miami P&B Investments’ accounting services and legal partner network can help buyers coordinate the right advisors before closing, not after a problem appears.

How Title Insurance Connects to Miami Condo Due Diligence

Many South Florida buyers are interested in condos because they offer lifestyle, security, amenities, rental potential, and easier lock-and-leave ownership.

That can be ideal for Canadian snowbirds and remote investors. But condo purchases require extra review.

Title insurance in Florida may help protect ownership rights, but it does not replace a careful review of the building itself. A clean title does not automatically mean the condo association is financially healthy, the building has strong reserves, rental rules fit your plan, or major repairs are fully funded.

For example, a buyer comparing Brickell Miami condos and Edgewater Miami condos should review both the unit-level title and the building-level risk profile.

A buyer looking at Aventura real estate or Coconut Grove real estate may face different questions around lifestyle, building age, association rules, assessments, parking, reserves, and long-term resale demand.

That is why title insurance should be part of a wider buyer checklist, not the only item on it.

What Canadian Buyers Should Know Before Closing from Abroad

Canadian buyers often have extra layers to manage.

You may be wiring funds across borders, signing remotely, reviewing documents from another time zone, coordinating with a U.S. lender, setting up insurance, arranging property management, and confirming tax reporting requirements.

Title insurance in Florida helps address ownership risk, but remote buyers also need a clean process.

Before closing, Canadian buyers should ask:

- Have all title requirements been cleared?

- Do I understand who pays each closing cost?

- Is my wire transfer timing realistic?

- Has my lender approved the final title documents?

- Have I reviewed the deed and ownership structure?

- Have condo or HOA balances been confirmed?

- Do I have local support after closing?

These questions matter whether you are buying a vacation condo, a long-term rental, a second home, or a property for future relocation.

If you are still early in your research, start with the full guide for Canadians buying property in Miami and the dedicated page for Miami real estate for Canadian investors.

Where Title Insurance in Florida Fits in the Buying Timeline

The best time to think about title insurance in Florida is before you are under pressure to close.

Here is a simple timeline:

| Stage | What to Review | Why It Matters |

|---|---|---|

| Before offer | Ownership records, property type, HOA risk, financing plan | Helps you avoid obvious red flags early |

| After contract | Title commitment, liens, title exceptions, association balances | Gives time to ask questions before closing |

| Before loan approval | Lender title requirements and closing instructions | Prevents financing delays |

| Before closing | Settlement statement, deed, policy details, wire instructions | Confirms costs and ownership details |

| After closing | Recorded deed, final policy, property management setup | Completes the ownership transition |

A common buyer mistake is waiting until the final week to review closing documents. By then, everyone may be focused on signing, wiring funds, and meeting deadlines.

A better approach is to ask early, review carefully, and bring in professional support when something is unclear.

Is Title Insurance Enough by Itself?

No. Title insurance in Florida is important, but it is not a complete investment strategy.

It does not tell you whether the property is priced well. It does not guarantee rental income. It does not inspect the roof, HVAC system, seawall, plumbing, windows, condo reserves, or insurance coverage. It does not solve exchange-rate risk. It does not replace legal, tax, accounting, or property management planning.

Think of title insurance as one layer of protection.

A strong South Florida purchase usually needs several layers: market guidance, property search, offer strategy, inspection review, title review, legal review, accounting input, insurance planning, HOA review, financing coordination, and post-closing management.

That is especially true across Miami, Fort Lauderdale, Boca Raton, and West Palm Beach, where property types, county customs, building conditions, and rental rules can vary significantly.

How Miami P&B Investments Helps Buyers Navigate Title and Closing Risk

Understanding title insurance in Florida is a smart step, but you do not have to handle the buying process alone.

Miami P&B Investments helps Canadian buyers, snowbirds, and South Florida investors connect the dots between property search, due diligence, closing, and long-term ownership.

If you are comparing properties, start with our main homes for sale in Miami Florida hub or explore location pages such as Miami real estate, Fort Lauderdale real estate, Boca Raton real estate, and West Palm Beach real estate.

From there, our real estate services can support the buying strategy, while our legal services, accounting services, property management, property maintenance, and construction services can help with the details that come before and after closing.

For Canadian snowbirds, our Canadian Snowbirds Realty page is a helpful starting point for lifestyle-focused buying. For investors, our Canadian investor resources can help you think through cash flow, ownership structure, tax coordination, management, and exit planning.

Title insurance in Florida is not the most exciting part of buying a Miami property. But it is one of the most important. When you understand what it does, what it does not do, and how it fits into the full closing process, you can buy with more confidence and fewer surprises.

If you are preparing to buy in Miami or South Florida and want a local team that understands both the Florida market and the needs of Canadian buyers, contact Miami P&B Investments to start the conversation.