Florida condo estoppel certificate due diligence is one of the most important closing steps many Miami and South Florida buyers do not fully understand until they are already under contract.

That can be risky.

A condo may look perfect in the listing photos. The view may be beautiful. The amenities may feel impressive. The rental estimate may look strong. But before closing, a buyer needs to know what the seller actually owes the association, whether transfer approval is required, whether special assessments are due, and whether any association-related issues could follow the unit into ownership.

That is where the estoppel certificate comes in.

For Canadian buyers, snowbirds, remote investors, and local South Florida buyers, this document can help confirm the financial status of the unit before money changes hands. It is not the same thing as a full condo document review, and it does not replace legal advice. But it can protect buyers from assuming the wrong numbers at one of the most sensitive points in the transaction.

If you are comparing condos in Miami, Brickell, Edgewater, Aventura, Coconut Grove, Fort Lauderdale, Boca Raton, or West Palm Beach, the Florida condo estoppel certificate should be part of your closing checklist.

What Is a Florida Condo Estoppel Certificate?

A Florida condo estoppel certificate is a written statement from the condominium association, or its authorized representative, that confirms key financial and association-related information about a specific unit.

In simple terms, it answers a closing question: what does this unit owe, what fees apply, and what association conditions must be handled before the buyer becomes the owner?

Buyers may hear different names for the same document. Some people call it a condo estoppel. Others call it an estoppel letter, association estoppel, HOA estoppel, or resale estoppel. In a Florida condominium purchase, the goal is the same: create a reliable snapshot of association-related amounts and requirements tied to the unit.

Unlike general marketing materials, the Florida condo estoppel certificate is not about selling the lifestyle of the building. It is about confirming numbers, deadlines, and association obligations. That is why it belongs in the same buyer conversation as Florida condo documents, the Florida condo questionnaire, title review, inspections, insurance, financing, and final closing costs.

Why This Document Matters Before Closing

A Florida condo estoppel certificate may look like routine paperwork, but it can reveal issues that directly affect your final decision.

For example, the seller may owe unpaid monthly assessments. A special assessment may be due soon. A transfer fee may apply. The association may require board approval before the sale closes. There may be an open violation noticed to the current owner. The building may also have a master association or additional association layer that creates extra fees.

These details matter because closing is not only about the purchase price.

A buyer who budgets only for the down payment, mortgage, taxes, and insurance may be surprised by association-related costs. This is especially important in South Florida, where condo buildings often have complex budgets, high insurance costs, amenities, reserves, security, elevators, garages, pools, staff, and long-term repair obligations.

If you are investing from Canada, the stakes can feel even higher. A $5,000 surprise in U.S. dollars can become a much larger planning issue once you convert it into Canadian dollars, wire funds internationally, and coordinate closing from another country. Miami P&B Investments’ page for Canadian investors buying in Miami and South Florida is a helpful place to understand how cross-border ownership adds extra layers to a purchase.

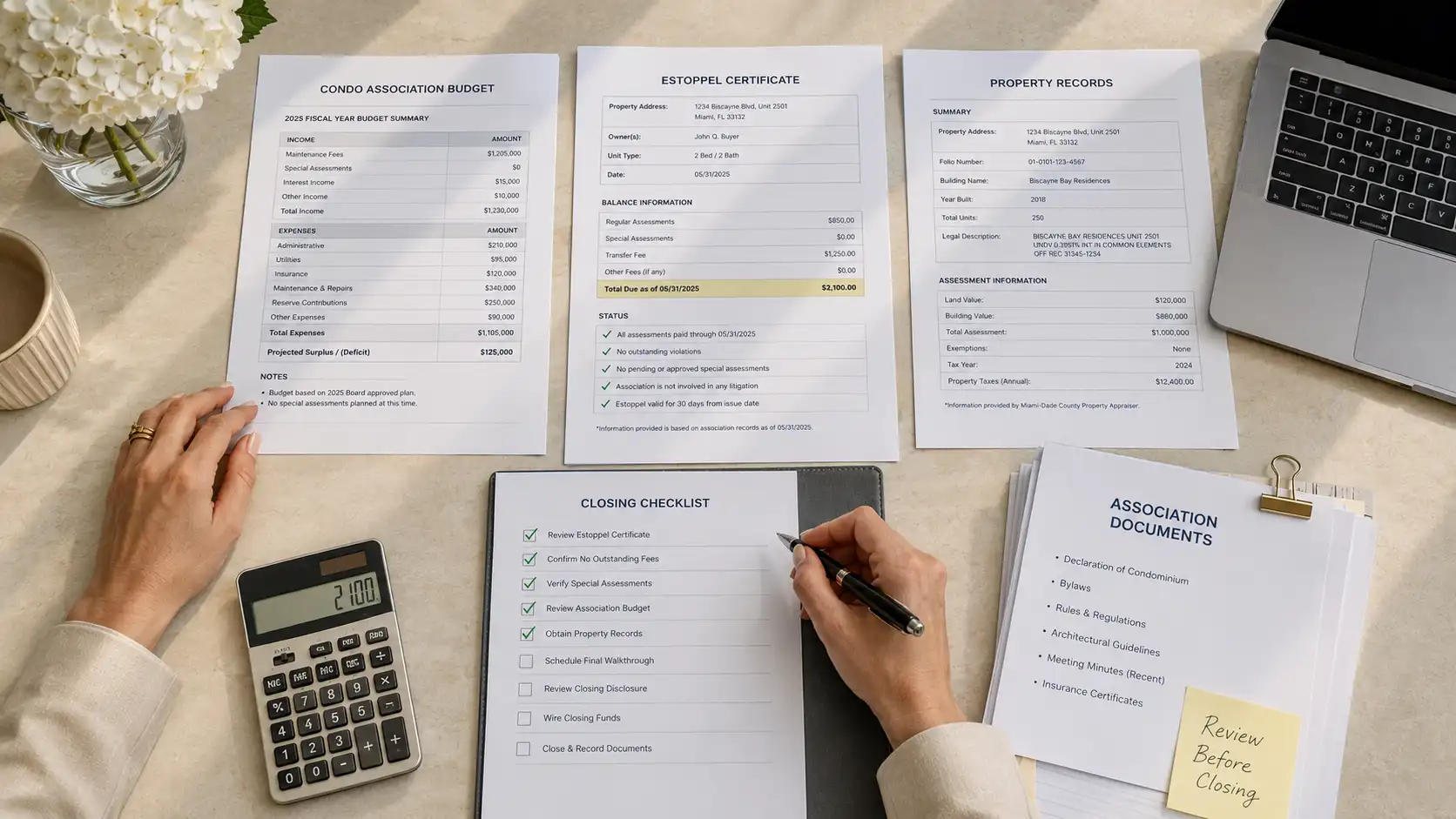

What a Florida Condo Estoppel Certificate Usually Shows

The Florida condo estoppel certificate typically includes a practical summary of association-related information. Buyers should not assume every certificate is equally easy to read, but the key items usually include:

| Estoppel item | Why buyers should care |

|---|---|

| Current owner and unit details | Confirms the certificate applies to the correct condo unit, parking space, and address. |

| Regular assessments | Shows the current monthly, quarterly, or periodic association fee. |

| Paid-through date | Confirms how far the seller has paid association dues. |

| Unpaid amounts | Identifies money owed by the seller to the association. |

| Special assessments | Shows current or scheduled extra charges that may affect ownership cost. |

| Transfer or resale fees | Helps buyers understand additional costs due at or near closing. |

| Open violations | Flags association rule issues noticed to the owner. |

| Transfer approval | Confirms whether board approval is required before the sale closes. |

| Association insurance contact | Helps buyers and lenders coordinate insurance review. |

This document does not tell you everything about the building. It should be read alongside the budget, financial statements, rules and regulations, declaration, bylaws, meeting minutes, reserve information, insurance details, and any engineering or inspection reports when available.

For a broader review process, read Miami P&B Investments’ guide to Florida condo reserve requirements and the article on Florida condo special assessments.

9 Smart Checks in a Florida Condo Estoppel Certificate

When the Florida condo estoppel certificate arrives, buyers should not simply file it away. Review it carefully with your real estate advisor, title company, attorney, lender, and accounting support when needed.

1. Confirm the unit, owner, and parking details

Start with the basics. Does the certificate match the correct property address, unit number, owner name, and parking or garage space?

This sounds simple, but mistakes can happen in large condo buildings with similar unit numbers, storage spaces, parking assignments, and multiple towers. If you are buying in a high-rise in Brickell, Edgewater, Downtown Miami, Aventura, or Sunny Isles, these details matter.

A parking space can affect value, rentability, convenience, and resale. A storage unit can also matter. Make sure the estoppel details line up with the purchase contract, MLS information, association records, and title work.

2. Review the regular assessment amount

The regular assessment is usually the recurring condo association fee. It may be monthly, quarterly, or structured another way.

Buyers should compare this number against the listing, seller disclosure, budget, and any HOA fee estimate used in their cash-flow analysis. If the amount is different, ask why.

For investors, even a modest difference can affect returns. A condo that looked profitable with a $900 monthly fee may look different if the actual fee is $1,175, especially after insurance, taxes, management, repairs, and vacancy are included. Miami P&B Investments’ guide to Miami rental cash flow can help buyers think beyond the listing price.

3. Check the paid-through date

The paid-through date tells you how far the seller has paid regular assessments.

If dues are paid through the end of the month, that may be simple. If the account is behind, the title company and closing team need to know how the unpaid amount will be handled. Most buyers do not want to inherit the seller’s unpaid association balance by accident.

This is one reason the Florida condo estoppel certificate is so important near closing. It helps clarify what needs to be collected, credited, or paid before the transaction is completed.

4. Look for unpaid assessments or collection issues

If the seller owes money to the association, the estoppel should identify amounts due. These may include unpaid dues, late fees, interest, collection costs, attorney involvement, or other association charges.

A buyer should ask a direct question: will all seller-related amounts be cleared at closing?

If the account has been turned over for collection, the closing process can become more complicated. That does not always mean the deal is impossible, but it does mean the buyer should slow down and make sure the title company and legal team are aligned.

5. Identify current and upcoming special assessments

Special assessments deserve careful attention.

Some assessments are already due. Others are approved but payable later. Some are being discussed but not finalized. The estoppel certificate may show current or scheduled amounts, but buyers should also review board minutes, budgets, notices, reserve studies, and recent owner communications to understand the bigger picture.

A simple example helps.

Imagine two condos are listed at similar prices. Unit A has no visible upcoming assessment. Unit B has a $35,000 special assessment payable over the next year. The purchase price alone does not tell the full story. Depending on the contract terms, seller negotiations, and timing, that assessment can change the true cost of the purchase.

This is why buyers should connect estoppel review with Miami HOA fee analysis and building-level due diligence.

6. Ask whether transfer approval is required

If the Florida condo estoppel certificate says transfer approval is required, do not ignore it.

Many associations require a buyer application, background check, interview, fee, orientation, or board approval before closing. Some buildings move quickly. Others need more time. If the approval process starts late, it can delay closing.

This is especially relevant for out-of-state and Canadian buyers who may need to provide documents remotely. If you are coordinating from Toronto, Montreal, Vancouver, Calgary, or elsewhere in Canada, ask early what the association needs, how documents must be submitted, and whether original signatures, notarization, or in-person steps are required.

7. Check for right of first refusal

Some associations have a right of first refusal. This means the association or its members may have a contractual right to match the offer or approve the transfer under the building’s governing documents.

Not every condo has this rule. But if it exists, your closing team needs to understand the procedure and timeline.

A right of first refusal does not automatically mean the buyer should walk away. It does mean the buyer should know whether the association has waived the right properly and whether all required notices have been handled before closing.

8. Review open violations

An open violation can create post-closing headaches.

Examples may include unauthorized alterations, balcony rules, flooring issues, pet violations, rental rule problems, storage violations, or changes made without association approval.

If a violation appears, ask what it is, who must cure it, how much it may cost, and whether the association will confirm resolution before closing. A small issue may be easy to fix. A larger issue may affect your renovation plans, insurance, rental strategy, or resale value.

Buyers planning to rent the property should also review Miami P&B Investments’ guide to Miami condo rental restrictions before assuming the unit will perform as expected.

9. Compare association information with official records

The estoppel certificate is important, but it should not be your only source of information.

Buyers can compare property details with the Miami-Dade Property Appraiser, recorded documents through the Miami-Dade Clerk Official Records, and legal requirements under the Florida Condominium Act. For a buyer-friendly industry explanation, the Florida Realtors overview of estoppel letters is also useful.

The goal is not to turn every buyer into a lawyer or title professional. The goal is to know when something does not line up.

Florida Condo Estoppel Certificate vs. Condo Questionnaire

Buyers often confuse the Florida condo estoppel certificate with the condo questionnaire. They are related to the same purchase, but they answer different questions.

A Florida condo estoppel certificate tells you what is owed to the association, what fees apply, whether approvals are needed, and whether certain association conditions exist for the specific unit.

A condo questionnaire is often more lender-focused. It usually helps the lender understand the building’s eligibility, insurance, reserves, litigation, owner occupancy, commercial use, deferred maintenance, rental concentration, and other project-level issues.

Both can matter. A buyer may personally qualify for financing, but the building may create concerns. Or the building may be financeable, but the specific unit may have unpaid assessments or transfer requirements that must be handled before closing.

For financed buyers, especially foreign national or Canadian buyers, timing is critical. Read the estoppel, questionnaire, title work, insurance information, and loan conditions together rather than treating each item as a separate checklist.

Why Canadian Buyers Should Pay Extra Attention

Canadian buyers should review the Florida condo estoppel certificate with one extra layer: currency and remote ownership planning.

Most condo costs are paid in U.S. dollars. That includes assessments, transfer fees, special assessments, insurance, repairs, closing costs, property management, and future maintenance. If the Canadian dollar moves, the real cost in CAD can change.

A Canadian buyer may also rely more heavily on local professionals because they are not physically present for every document request, board communication, or closing update. This makes organization especially important.

Ask these practical questions early:

- Are all association balances paid or being cleared at closing?

- Are any special assessments due after closing?

- Does the association require approval before transfer?

- Can the buyer submit documents electronically?

- Are rental rules compatible with the ownership plan?

- Will ongoing ownership costs still make sense after CAD-to-USD conversion?

Canadian snowbirds who plan to use the condo seasonally should also consider how rules affect guests, family use, pets, parking, storage, and maintenance access. Miami P&B Investments’ Canadian Snowbirds Realty page is a helpful starting point for buyers who want a winter home that is also practical to own from Canada.

When Should Buyers Review the Estoppel?

The estoppel is usually ordered during the closing process, but buyers should think about association risk much earlier.

Before making an offer, ask about HOA fees, known assessments, rental rules, building age, insurance, reserves, milestone inspections, and whether the building has any known financing concerns. Once under contract, make sure your closing team orders and reviews association documents on time.

The biggest mistake is waiting until the final days before closing to discover a fee, approval requirement, violation, or assessment that should have been discussed earlier.

A strong buyer process looks like this:

- Screen the building before making an offer.

- Review condo documents during the contract period.

- Confirm financing and insurance requirements early.

- Study the condo questionnaire if a lender is involved.

- Review the estoppel before closing funds are finalized.

- Resolve open association issues before ownership transfers.

This process helps buyers protect their deposit, closing timeline, and long-term ownership plan.

Common Buyer Mistakes With Condo Estoppel Review

One common mistake is assuming that the association fee shown in the listing is automatically correct. Listings can contain outdated information, and association fees can change. The Florida condo estoppel certificate gives buyers a more direct confirmation near closing.

Another mistake is focusing only on unpaid dues while ignoring upcoming charges. A seller may be current today, but a special assessment may still be due after closing. Buyers should understand both current balances and future obligations.

A third mistake is treating transfer approval as a minor detail. If the association requires approval, the buyer should know the timeline, fees, documents, and process as early as possible. Waiting too long can create unnecessary stress close to closing day.

Finally, buyers should avoid reviewing the estoppel in isolation. The document is most useful when it is compared against the purchase contract, title work, budget, association rules, insurance information, inspection details, and ownership strategy.

How Miami P&B Investments Helps Buyers Review Condo Closing Risk

A Florida condo estoppel certificate should not be treated as a formality. It is part of the final reality check before you own the unit.

At Miami P&B Investments, buyers receive practical guidance that connects the listing, building, association documents, closing process, and long-term ownership strategy. That matters whether you are a local buyer, a U.S. investor, a Canadian snowbird, or a remote investor purchasing from another country.

Our team can help you compare buildings, review ownership costs, coordinate with trusted professionals, and understand how association details may affect your purchase. Through our real estate services, property management support, legal service coordination, accounting guidance, property maintenance services, and construction support, we help buyers look beyond the listing and understand what ownership may actually feel like after closing.

If you are considering a condo in Miami or South Florida, start with the right questions before you fall in love with the view. Review the building, the rules, the costs, the rental plan, and the estoppel details with a team that understands the local market.

To discuss your next purchase, visit Miami P&B Investments’ services page or contact the team for personalized guidance before you move forward.