Florida condo reserve requirements are now one of the most important things buyers should understand before purchasing a condo in Miami, Fort Lauderdale, Boca Raton, West Palm Beach, Aventura, Brickell, Edgewater, Coconut Grove, Bay Harbor Islands, or anywhere else in South Florida.

For years, many buyers focused mainly on location, view, amenities, monthly HOA fees, and rental potential. Those details still matter. But in today’s market, the financial health of the building can be just as important as the unit itself.

A beautiful condo in a weak association can create surprise costs, financing delays, lower resale demand, or special assessment risk. A less flashy unit in a well-funded, well-managed building may offer a stronger long-term ownership experience.

This matters for local buyers. It matters even more for Canadian buyers and investors purchasing from Toronto, Vancouver, Montreal, Calgary, or elsewhere in Canada. When your expenses are in U.S. dollars, every increase in HOA dues, reserve contributions, or assessments can feel larger once converted back into Canadian dollars.

This guide explains what Florida condo reserve requirements mean, why they matter in 2026, and how to review them before making an offer.

What Florida Condo Reserve Requirements Really Mean

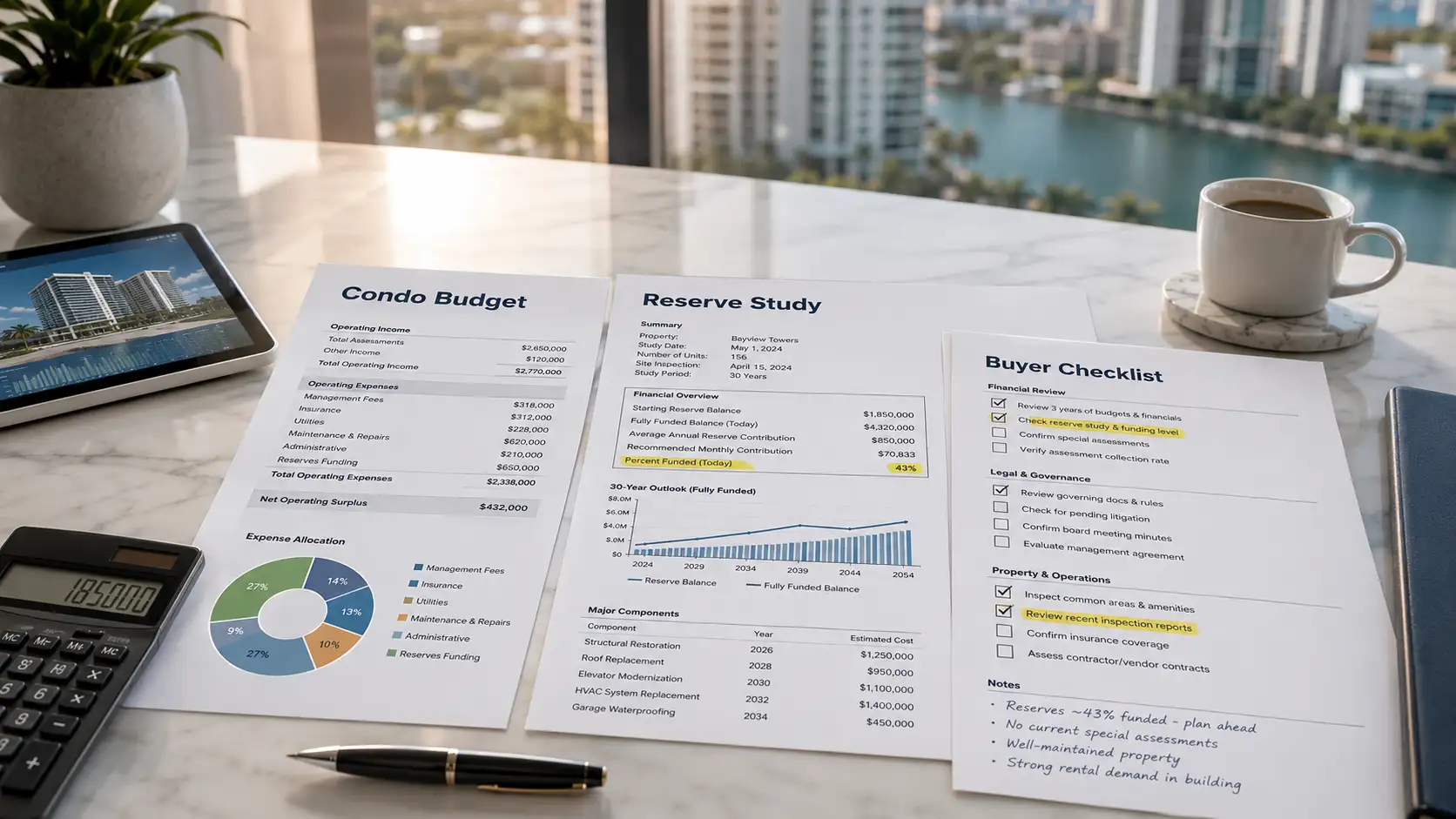

Florida condo reserve requirements are rules that affect how condominium associations plan and fund future repairs, replacements, and major building maintenance.

In simple terms, a condo association should not only collect enough money to pay current bills. It also needs to prepare for future building needs. Roofs age. Waterproofing wears down. Plumbing and electrical systems need upgrades. Windows, doors, fire protection systems, structural components, and exterior surfaces all require long-term planning.

That planning usually shows up through the building’s reserve study, annual budget, financial statements, and board decisions.

For many South Florida condo buildings, especially taller buildings, the conversation now includes the Structural Integrity Reserve Study, often called SIRS. Buyers do not need to become engineers or lawyers, but they do need to understand what the report says, whether the association is funding reserves properly, and whether future costs could affect ownership.

If you are still early in your research, Miami P&B Investments’ guide for Canadian investors buying in Miami and South Florida is a helpful starting point. Then use this article to focus specifically on reserves and building-level risk.

Why Florida Condo Reserve Requirements Matter More in 2026

Florida condo reserve requirements matter more now because buyers are looking at a different condo market than they were a few years ago.

Associations are paying closer attention to long-term repairs, structural inspections, insurance, reserve funding, and maintenance history. Lenders are also asking tougher questions about condo buildings before approving loans. That means the building itself can affect whether a buyer gets financing, how much the property costs to own, and how easy it may be to sell later.

The practical question for a buyer is not only, “Do I like this condo?”

The better question is, “Does this building have a realistic plan to maintain itself over time?”

That one question can protect you from buying into an association that looks affordable today but may become expensive tomorrow.

For example, a building with low monthly HOA fees may appear attractive at first. But if the fees are low because reserves were underfunded for years, the association may eventually need a large special assessment, loan, or sharp monthly increase. On the other hand, a building with higher monthly dues may actually be more stable if those dues support proper reserves, insurance, security, amenities, and maintenance.

That is why Florida condo reserve requirements should be reviewed together with Miami HOA fees, insurance, rental rules, taxes, financing, and your long-term investment plan.

Reserve Requirements vs HOA Fees vs Special Assessments

Buyers often confuse reserves, HOA fees, and special assessments. They are connected, but they are not the same thing.

HOA fees are the regular monthly or quarterly payments owners make to the association. These fees may cover building staff, insurance, utilities, amenities, landscaping, cleaning, security, management, and reserve contributions.

Reserves are funds set aside for future repairs and replacements. They are not supposed to be treated like everyday spending money. Healthy reserves help the association plan ahead instead of reacting with emergency costs later.

Special assessments are additional charges owners may need to pay when the association does not have enough money for a major expense, repair, insurance increase, legal issue, or improvement project.

Here is the simple way to think about it:

| Cost Item | What It Means | Why Buyers Should Care |

|---|---|---|

| HOA fees | Recurring owner payments | Affects monthly cash flow and affordability |

| Reserves | Money saved for future building needs | Shows whether the association is planning ahead |

| Special assessments | Extra owner charges beyond regular fees | Can create major surprise costs after closing |

A strong buyer review looks at all three. Florida condo reserve requirements are not just a technical issue. They are part of the real cost of ownership.

For a deeper look at assessments, Miami P&B Investments’ guide to Florida condo special assessments is a useful companion article.

The 7 Checks Buyers Should Make Before Offering

Before making an offer on a Miami or South Florida condo, buyers should review Florida condo reserve requirements through a practical checklist. The goal is not to reject every building with upcoming repairs. The goal is to understand the cost, timing, and risk before you commit.

1. Ask Whether the Building Has a Current Reserve Study

The first step is simple: ask for the most current reserve study and any Structural Integrity Reserve Study if applicable.

A reserve study helps estimate future repair and replacement needs. It should show what major building components may need attention, how much those projects could cost, and how the association plans to fund them.

If the association cannot provide clear reserve information, that does not automatically mean the condo is a bad purchase. But it does mean you need more due diligence before moving forward.

Buyers can also review official state information on Florida SIRS reporting to understand how the state describes these studies and reporting expectations.

2. Compare the Reserve Study to the Annual Budget

A reserve study is only useful if the budget responds to it.

If the study recommends stronger annual contributions but the association budget does not reflect those needs, buyers should ask why. The issue may be timing, updated repairs, loans, board strategy, or member decisions. But the gap needs to be explained.

This is where Florida condo reserve requirements become practical. You are not only reading a report. You are checking whether the association is acting on the information.

A good buyer question is: “Does the current budget fund reserves according to the most recent study?”

If the answer is unclear, ask for meeting minutes, board explanations, updated budgets, and any notices sent to owners.

3. Look for Zero-Life or Urgent Repair Items

Some reserve studies identify components with little or no remaining useful life. That can be a serious clue.

It does not always mean the building is unsafe. It may mean a roof, waterproofing system, mechanical system, or other component is due for repair or replacement soon. But if the association has not planned how to pay for that work, the buyer may inherit future costs.

When reviewing Florida condo reserve requirements, pay close attention to items that appear urgent, underfunded, repeated in board minutes, or tied to inspection findings.

If a report mentions major concrete restoration, waterproofing, window replacement, balcony repairs, plumbing replacement, or fire system upgrades, ask how those projects will be funded.

4. Review Board Minutes for Future Cost Signals

Board minutes often reveal what polished marketing materials do not.

They may show discussions about rising insurance, delayed repairs, owner complaints, engineering reports, contractor bids, budget pressure, legal issues, or potential special assessments.

If a building is considering a major project, the minutes may show early warning signs months before a formal assessment is issued.

This is why buyers should not rely only on the listing, the seller disclosure, or the monthly HOA amount. A complete review includes the documents behind the building. Miami P&B Investments’ article on Florida condo documents explains how to turn those records into a useful buying decision.

5. Check Whether the Building Is Financeable

Florida condo reserve requirements can affect financing.

Lenders often review the building’s budget, insurance, reserves, delinquency levels, owner occupancy, litigation, deferred maintenance, and association answers to the condo questionnaire. If the building raises too many concerns, the buyer may face delays, higher down payment requirements, non-warrantable condo issues, or fewer lending options.

This is especially important for Canadian buyers using cross-border financing. You may be financially strong as a borrower, but the building still needs to pass lender review.

If financing matters to your purchase, review the building early. Do not wait until the final days of the loan process to discover that the lender has concerns about reserves or deferred maintenance.

For more detail, read Miami P&B Investments’ guide on Florida condo questionnaires and the article on non-warrantable condos in Florida.

6. Understand the Relationship Between Reserves and Insurance

Insurance and reserves are separate issues, but they often move together in South Florida.

A building with older systems, deferred maintenance, coastal exposure, or unresolved repairs may face higher insurance costs. Higher insurance costs can increase monthly HOA fees. If insurance and repair costs rise at the same time, the association may need to adjust budgets more aggressively.

That is why Florida condo reserve requirements should be reviewed alongside insurance history and current coverage.

Before your inspection period ends, ask what insurance coverage the building carries, whether premiums recently increased, whether wind or flood exposure affects costs, and whether owners need separate policies. For flood exposure, buyers can also review the FEMA Flood Map Service Center as part of broader due diligence.

Miami P&B Investments’ guides to Miami property insurance costs and Miami flood zones can help you understand this part of the ownership picture.

7. Estimate the True Cost in Both USD and CAD

For Canadian buyers, Florida condo reserve requirements have a currency layer.

If HOA dues increase by $300 per month, that is $3,600 per year in U.S. dollars. Once converted into Canadian dollars, the impact depends on the exchange rate. If a special assessment arrives, the currency effect can be even more noticeable.

That does not mean Canadians should avoid Miami condos. Many Canadian buyers still prefer South Florida for lifestyle, rental demand, diversification, climate, and long-term property ownership. But the math should be clear before closing.

Build a simple ownership model that includes purchase price, mortgage payment if applicable, HOA fees, reserve-related increases, property taxes, insurance, management, maintenance, vacancy, accounting, legal setup, and currency movement.

If your goal includes rental income, compare your reserve assumptions with a realistic rental projection. Miami P&B Investments’ guide to Miami rental cash flow can help you think through that full cost stack.

How Florida Condo Reserve Requirements Affect Different Buyer Types

Not every buyer experiences Florida condo reserve requirements the same way.

A cash buyer may care most about long-term cost stability and resale. A financed buyer may care about lender approval. A Canadian investor may care about currency, rental income, and remote management. A snowbird may care about predictable seasonal ownership. A full-time resident may care about monthly affordability and building maintenance.

For a rental investor, reserve funding affects cash flow. Higher HOA fees reduce net income, but better reserves may reduce future surprise costs. For a lifestyle buyer, reserves affect peace of mind. You want to enjoy the property without worrying about constant building emergencies. For a resale-focused buyer, reserves can affect future buyer confidence.

Strong buildings tend to document things clearly. They may not always be cheap, but they are easier to understand. Weak buildings often require more negotiation, more caution, and more professional review.

If you are comparing neighborhoods, reserve issues may show up differently. High-rise condo markets like Brickell, Edgewater Miami, and Aventura may involve detailed building-level reviews. Boutique or waterfront areas like Bay Harbor Islands and Coconut Grove may have different association structures, amenities, and maintenance needs.

The right choice depends on your budget, timeline, financing, rental plans, and risk tolerance.

Do Newer Condos Avoid Reserve Problems?

Not always.

Newer buildings may have fewer immediate age-related repairs, but buyers still need to review budgets, warranties, turnover status, developer control, maintenance plans, insurance, and future reserve needs.

A new building with luxury amenities can have high operating costs. Pools, spas, elevators, valet areas, fitness centers, glass exteriors, waterfront decks, and advanced mechanical systems all require long-term maintenance.

Older buildings may have more visible repair needs, but some are well-managed and financially disciplined. Newer buildings may look perfect but still need careful review.

That is why Florida condo reserve requirements should be part of every condo purchase, not only older tower purchases.

If you are considering a new development or resale alternative, Miami P&B Investments’ article on Miami pre-construction condos for Canadian investors can help you compare timelines, risks, and ownership planning.

What Buyers Should Ask During Due Diligence

During the inspection or document review period, buyers should ask direct questions. Clear answers can reduce uncertainty. Vague answers should lead to more review.

Useful questions include:

- Does the building have a current reserve study or SIRS?

- When was it completed?

- What major components are listed for near-term repair or replacement?

- Are reserves being funded according to the most recent study?

- Has the association discussed a special assessment, loan, or line of credit?

- Have HOA fees increased recently?

- Are there upcoming budget changes?

- Is there any deferred maintenance?

- Are there open insurance issues or claim disputes?

- Has the building completed required inspections?

- Do lenders currently finance units in the building?

Buyers can also review the Florida Condominium Act reserve and structural integrity study language for official legal context, but professional guidance is important because every building and transaction is different.

This is also where local experience matters. A document may be technically available but difficult to interpret. A building may look risky at first but have a reasonable funding plan. Another building may look clean but have unresolved issues hidden in minutes, budgets, or association communication.

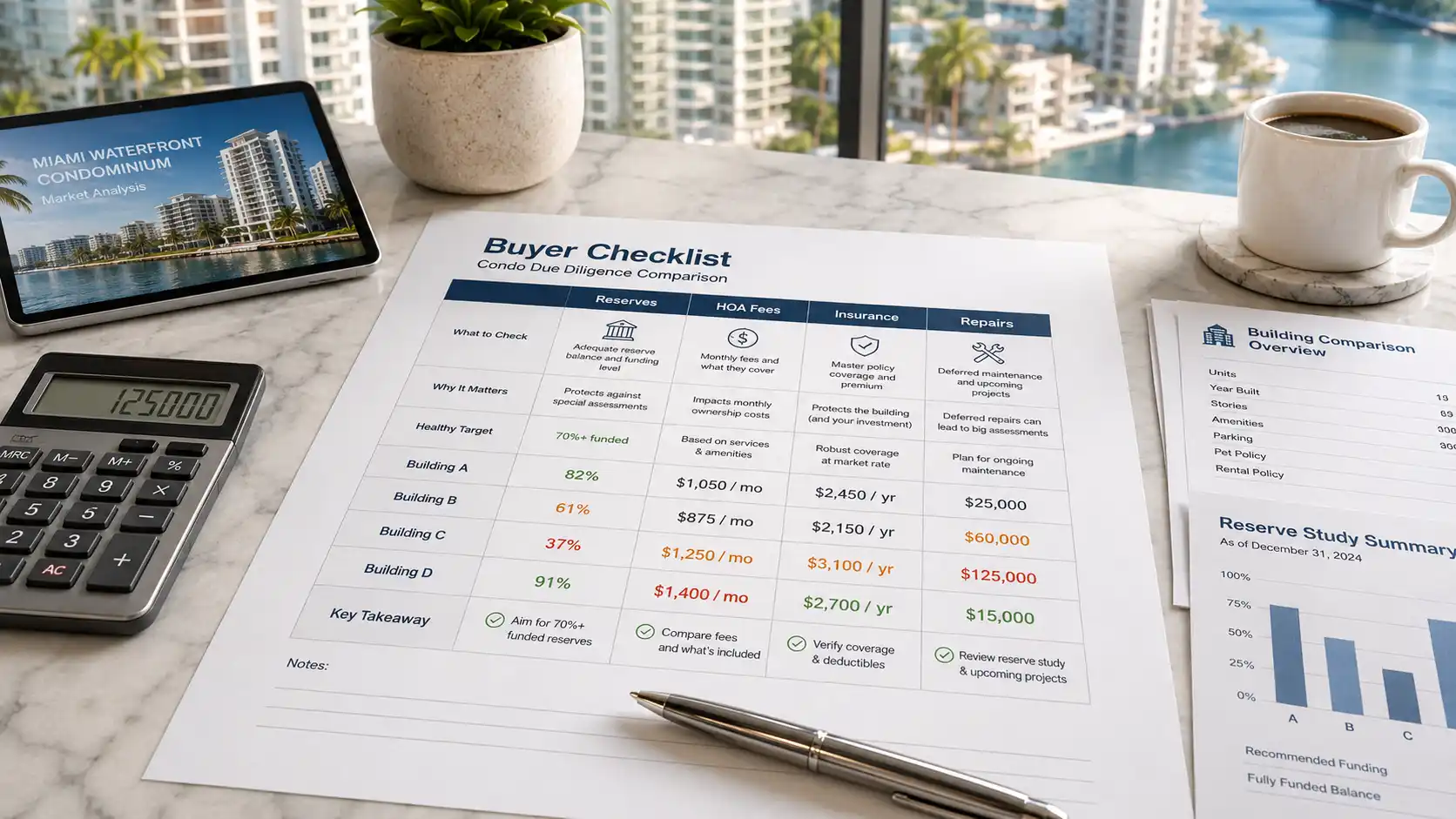

How to Compare Two Miami Condos Using Reserve Information

Imagine two similar condos in Miami.

Condo A has a lower monthly HOA fee, older building systems, limited reserve contributions, and vague board minutes about future repairs. The view is excellent, and the purchase price looks attractive.

Condo B has a higher HOA fee, clearer reserves, completed inspections, transparent budgets, and fewer unknowns. The unit is slightly more expensive, but the association has a more organized plan.

Which one is better?

The answer depends on your goals. Condo A may offer negotiation opportunity if the seller discounts the price enough and the buyer understands the risk. Condo B may offer more predictability, easier financing, and stronger peace of mind.

The mistake is choosing only by purchase price or HOA fee.

Florida condo reserve requirements help buyers compare the building behind the unit. That comparison can reveal whether a “deal” is truly a deal or whether the lower price is simply reflecting higher future risk.

Build a Smarter Condo Plan With Miami P&B Investments

Florida condo reserve requirements are not meant to scare buyers away from Miami or South Florida condos. They are meant to help buyers make better decisions.

For Canadian buyers, snowbirds, investors, and local South Florida buyers, the strongest approach is simple: review the unit, the building, the association, the documents, the numbers, and the long-term plan before you commit.

At Miami P&B Investments, our team helps buyers look beyond the listing photos. Through our real estate services, we help you compare buildings, neighborhoods, pricing, rental potential, and ownership goals. Through our property management services, we support remote owners who want hands-off oversight after closing. Our property maintenance services help protect the condition of your unit, while our trusted legal and accounting partners can help you understand contracts, entity structure, taxes, reporting, and cross-border ownership details.

If you are browsing condos in Miami, Fort Lauderdale, Boca Raton, West Palm Beach, or another South Florida market, start by reviewing the property and the building together.

When you are ready to compare real options, explore current listings through Miami P&B Investments’ home search or contact our team for a personalized buying plan.

The right Miami condo is not only the one with the best view. It is the one that fits your lifestyle, your numbers, your risk tolerance, and your long-term strategy.