Florida condo questionnaire review can decide whether a Miami condo purchase moves smoothly toward closing or turns into a last-minute financing problem.

Many buyers focus on the unit first. They compare the view, balcony, amenities, parking, price, and neighborhood. Those details matter. But for financed condo purchases, the lender also cares about the building itself.

That is where the Florida condo questionnaire becomes important.

For Canadian buyers, snowbirds, and South Florida investors, this document can reveal issues that are not obvious in listing photos. It can point to reserve gaps, insurance problems, litigation, deferred maintenance, rental limitations, special assessments, commercial use, or project eligibility concerns that may affect financing and long-term ownership.

If you are comparing condos in Brickell, Edgewater, Aventura, Coconut Grove, Miami Beach, Fort Lauderdale, Boca Raton, or West Palm Beach, this guide explains what the questionnaire does, why it matters, and what to review before you remove contingencies.

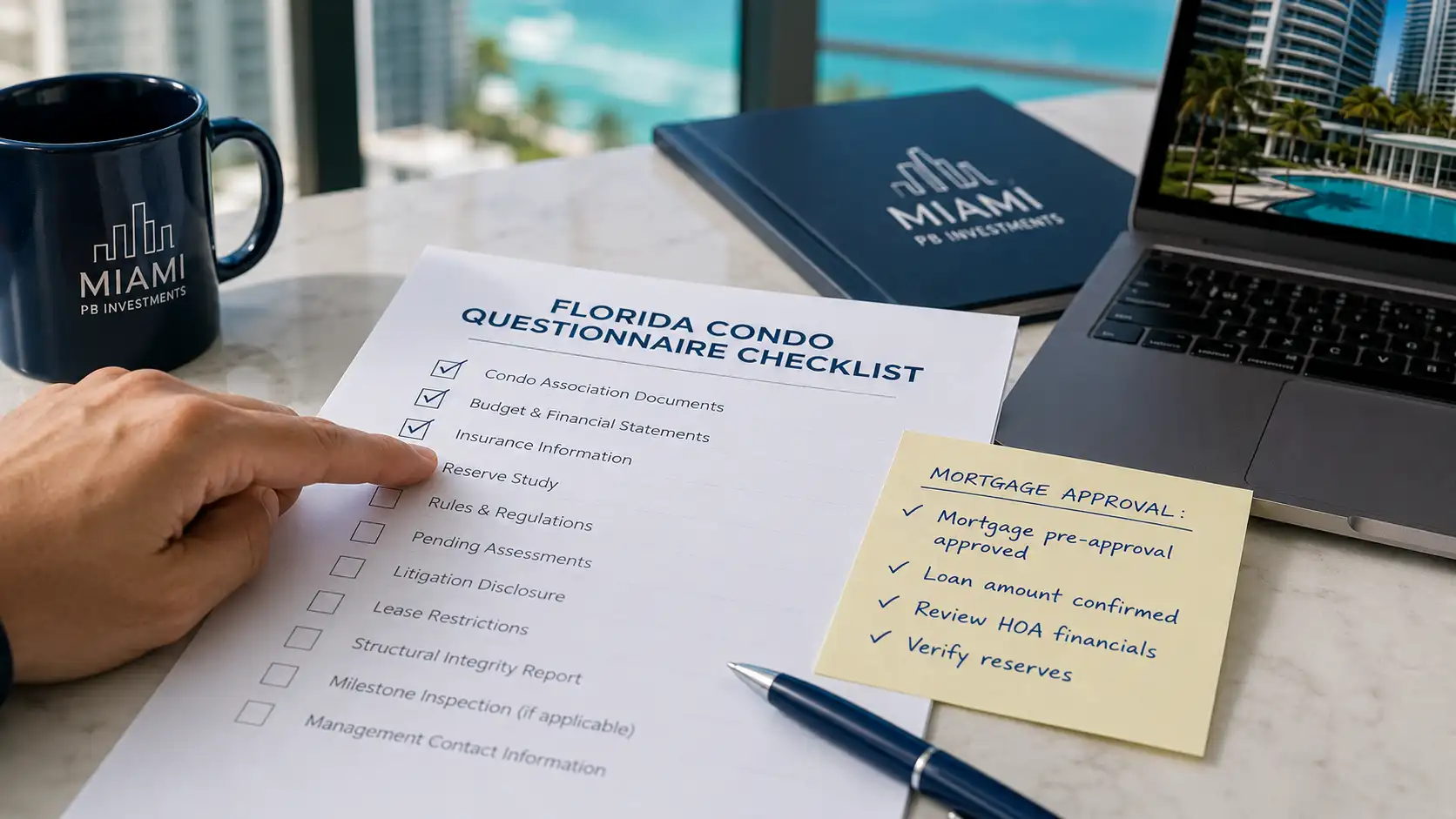

What Is a Florida Condo Questionnaire?

A Florida condo questionnaire is a lender-facing document completed by the condominium association, management company, or authorized representative.

Its purpose is simple: the lender wants to understand whether the building is a safe, financeable project before approving a loan secured by one unit inside that building.

Think of it as a building-level risk report.

A buyer may qualify personally. Their credit may be strong. Their down payment may be ready. Their income may be verified. But if the condo project itself raises concerns, the lender may pause, request more documentation, change loan terms, or decline the file.

That is why this document belongs beside your Florida condo documents review, your Miami HOA fees analysis, and your financing plan.

Why the Florida Condo Questionnaire Matters More in 2026

Florida condos are under more scrutiny than they were a few years ago. Lenders, insurers, associations, and buyers are all paying closer attention to reserves, insurance, structural condition, and future repair costs.

This is especially true in South Florida, where many desirable buildings are coastal, high-rise, amenity-heavy, and exposed to wind, flood, salt air, and rising insurance costs.

The Florida condo questionnaire matters because it connects the buyer’s mortgage approval to the building’s financial and physical condition. A beautiful unit in a weak building can create financing friction. A simpler unit in a well-managed building may be easier to finance and own.

For Canadians, the stakes can feel even higher. You may be moving money from CAD to USD, coordinating documents across borders, and relying on a local team to catch issues before your deposit, travel plans, or closing timeline are at risk. For a broader financing overview, see Miami P&B Investments’ guide to a U.S. mortgage for Canadians in Florida.

What Lenders Are Trying to Learn

A Florida condo questionnaire usually looks beyond the individual unit. The lender is trying to answer practical questions such as:

Is the project mostly residential?

Are enough units sold and owner-controlled?

Is the association financially stable?

Are reserves being funded?

Is there major litigation?

Is there deferred maintenance or structural concern?

Are there special assessments?

Does the insurance coverage meet lender requirements?

Are rentals, commercial space, or investor ownership creating risk?

This is why buyers should not treat the Florida condo questionnaire as routine paperwork. It can be the difference between a clean loan approval and a stressful closing delay.

1. Confirm the Type of Project and Ownership Control

The first buyer check is basic but important: what kind of condo project are you buying into?

A lender may look at whether the project is new construction, newly converted, established, still developer-controlled, mixed-use, or part of a larger master association. These details can affect review type, documentation, and financing options.

For example, a resale condo in an established Brickell tower may be reviewed differently from a new development where the developer still controls the association. A boutique Coconut Grove building may have a different profile from a large Edgewater high-rise with multiple associations.

If you are still deciding where to buy, compare location pages such as Brickell real estate, Edgewater Miami real estate, Coconut Grove real estate, and Aventura real estate. The neighborhood matters, but the building structure matters just as much.

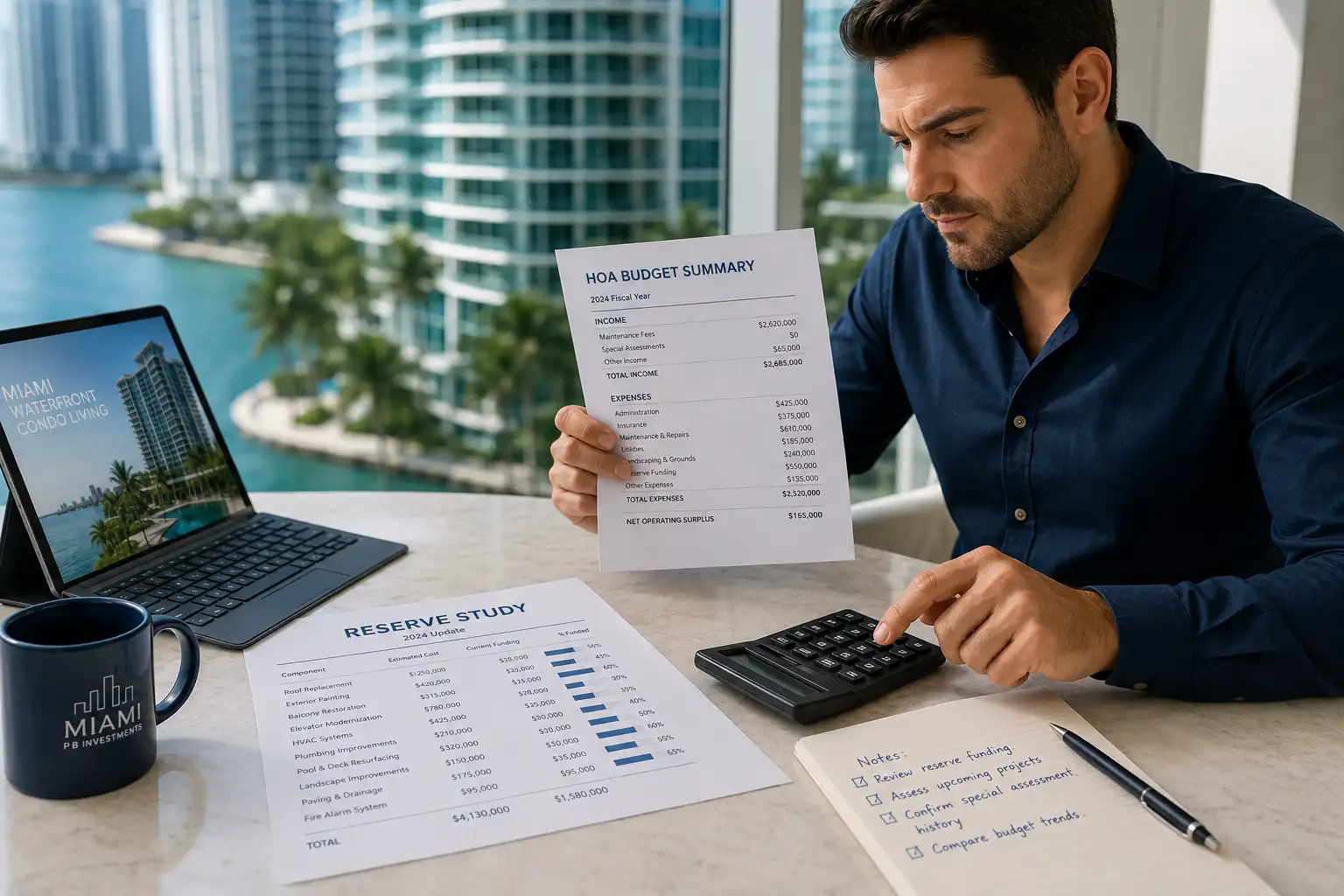

2. Review Reserves and Financial Controls

The second major area is the association’s financial health.

A Florida condo questionnaire may ask about reserve accounts, operating accounts, budget practices, financial controls, reserve studies, and whether funds are separated properly.

This matters because reserves are the building’s future repair fund. If reserves are too low, the association may need higher monthly dues, special assessments, or loans to pay for major work.

A low HOA fee may look attractive at first. But if the building is underfunded, that low fee can become expensive later. This is why buyers should compare the questionnaire against the budget, year-end financials, board minutes, and reserve information.

A useful buyer question is: does the association look proactive or reactive?

A proactive association plans ahead, funds reserves, communicates clearly, and documents major repairs. A reactive association waits until problems become urgent. For investors, that difference can affect cash flow, resale value, and tenant satisfaction.

3. Check Insurance, Flood Exposure, and Deductibles

Insurance is one of the biggest pressure points in South Florida condo ownership.

The Florida condo questionnaire may ask for hazard, liability, fidelity, and flood insurance information. It may also ask whether units or common elements are in a flood zone and whether coverage meets required standards.

For Miami and coastal buyers, this section should not be skipped.

A building’s master policy does not automatically cover everything inside your unit. You may still need your own unit policy. You may also face deductibles, exclusions, or loss assessment exposure after a major event.

If you are buying near the water, pair this review with Miami P&B Investments’ guide to Miami flood zones and the official Fannie Mae condo, co-op, and PUD eligibility resources. The goal is not to become an underwriter. The goal is to know which questions to ask before financing depends on the answers.

4. Look Closely at Structural Safety and Deferred Maintenance

In Florida, structural condition has become a major part of condo due diligence.

A Florida condo questionnaire may ask when the last building inspection occurred, whether there were findings related to safety or structural integrity, whether recommended repairs were completed, and whether any deferred maintenance remains.

This is where buyers should slow down.

A “yes” answer does not always mean you should walk away. Buildings need repairs. Coastal towers need maintenance. Older properties can still be excellent purchases when issues are identified, funded, and managed properly.

The problem is uncertainty.

If the questionnaire says repairs remain, ask what they are, how much they cost, who is paying, when they will be completed, and whether the work affects financing, insurance, occupancy, amenities, or resale.

For additional context, review Florida condo special assessments and the state’s DBPR condominium information resources, which explain Florida’s broader push toward safety, transparency, and responsible condo management.

5. Identify Current or Planned Special Assessments

Special assessments deserve their own buyer check.

The Florida condo questionnaire can ask whether current or planned assessments exist, how much they are, what terms apply, and what purpose they serve.

This matters for both financing and ownership.

For a financed buyer, the lender may want to know whether the assessment is affordable, whether it signals deeper building issues, and whether it affects the project’s eligibility. For a cash buyer, the same assessment still affects total cost, return on investment, and exit strategy.

Here is a simple example.

A condo listed at $650,000 may look better than a similar unit listed at $690,000. But if the first building has a pending $45,000 assessment and unclear repair timing, the cheaper unit may not be cheaper at all.

This is why a serious offer should be based on the full building picture, not only the list price.

6. Understand Rentals, Commercial Space, and Investor Concentration

Many Canadian and out-of-state buyers want flexibility. They may use the condo for winter months, rent it seasonally, or hold it as a long-term investment.

The Florida condo questionnaire can reveal whether the project includes commercial space, hotel-like operations, short-term rental activity, or a high concentration of investor-owned units.

This connects directly to your use plan.

If your goal is rental income, confirm the building rules before you assume anything. Some buildings allow annual leases only. Others allow 30-day minimum rentals. Some restrict the number of leases per year. Some require board approval. Some are simply not designed for short-term rental strategies.

A lender may care about these answers, and you should too. For a deeper rental rules review, see Miami P&B Investments’ guide to Miami condo rental restrictions.

7. Time the Questionnaire Early Enough to Protect Closing

The Florida condo questionnaire can become a problem when it is ordered too late.

By the time a buyer is under contract, several clocks are already moving. Inspection periods, financing contingencies, appraisal timing, association approval, title work, insurance review, and closing deadlines all overlap.

If the questionnaire uncovers issues late, your options shrink.

The better approach is to screen buildings before you make an offer whenever possible. Ask your agent and lender whether the building has known financing concerns. Review recent sales. Look for signs of non-warrantable status. Ask whether similar buyers recently closed with financing.

Miami P&B Investments’ article on non-warrantable condos in Florida is a helpful next read because it explains what can happen when a building does not meet standard financing guidelines.

Do Cash Buyers Still Need to Care?

Yes.

A cash buyer may not need a lender to approve the project, but the Florida condo questionnaire can still reveal valuable risk signals.

If future buyers cannot easily finance units in the building, your resale pool may be smaller. If reserves are thin, your carrying costs may rise. If insurance is weak, you may face higher risk. If deferred maintenance is unresolved, you may inherit uncertainty.

Cash gives you speed and negotiating power. It does not replace due diligence.

For Canadians buying in cash, the question is not only “Can I close?” It is “Will this building still make sense when I own it, manage it, rent it, and eventually sell it?”

A Mini Buyer Checklist Before You Remove Contingencies

Use this quick breakdown when reviewing a condo purchase:

| Review Area | What to Check | Why It Matters |

|---|---|---|

| Project type | New, established, conversion, mixed-use | Affects lender review |

| Reserves | Funding, reserve study, account controls | Shows long-term planning |

| Insurance | Hazard, flood, liability, deductibles | Affects financing and risk |

| Repairs | Inspections, deferred maintenance, timelines | Can delay loans or increase costs |

| Assessments | Current, planned, amount, purpose | Changes true purchase price |

| Rental rules | Minimum lease term, approvals, limits | Impacts income strategy |

| Timing | Order early, review before deadlines | Protects closing leverage |

This table is not a substitute for legal, lending, or accounting advice. It is a practical way to organize the conversation with your team.

How Canadian Buyers Should Read the Numbers

Canadian buyers should add one extra step: convert the ownership picture into Canadian dollars.

The Florida condo questionnaire may reveal a higher HOA fee, upcoming assessment, insurance gap, or repair plan. Each of those costs is usually paid in USD. A manageable number in U.S. dollars can feel very different after exchange rate movement.

That is why cross-border buyers should build a full cost stack before closing:

Purchase price.

Down payment and closing costs.

HOA fees.

Property taxes.

Insurance.

Potential assessments.

Property management.

Repairs and maintenance.

Accounting and tax filing support.

For tax-related planning, review Florida property taxes for non residents and Miami P&B Investments’ accounting services. The financing document is only one part of the bigger ownership plan.

What If the Florida Condo Questionnaire Raises Red Flags?

A red flag is not always a deal breaker. Sometimes the Florida condo questionnaire simply shows that the lender needs more context.

For example, an association may have a special assessment, but the work may already be funded and nearly complete. A building may show deferred maintenance, but the repairs may be documented, permitted, and scheduled. A flood insurance question may need clarification from the master policy rather than a full loan restructure.

The key is not to panic. The key is to pause, gather the missing documents, and compare the Florida condo questionnaire with the budget, minutes, insurance package, reserve study, and association disclosures.

If the answers remain vague, that is when the Florida condo questionnaire becomes more than a form. It becomes a warning to renegotiate, request credits, extend timelines, switch financing strategy, or move to a stronger building.

How Miami P&B Investments Helps Buyers Use the Florida Condo Questionnaire

The Florida condo questionnaire is not just paperwork. It is a decision tool. In practice, the Florida condo questionnaire should be reviewed before emotions, deadlines, or exchange-rate pressure take over. When reviewed early, the Florida condo questionnaire can help buyers avoid weak buildings and focus on stronger opportunities.

At Miami P&B Investments, we help buyers look beyond the unit and evaluate the building behind it. That means reviewing financing risk, HOA health, reserves, insurance, rental rules, special assessments, maintenance history, and long-distance ownership needs before you commit.

For Canadian buyers, this is especially valuable. You need a local team that understands South Florida condo buildings, foreign-national financing, CAD-to-USD planning, remote closings, and after-closing support.

Our real estate services can help you compare the right buildings. Our legal services can help coordinate contract and document review. Our property management services can support hands-off ownership after closing. Our property maintenance and construction services can help protect the asset over time.

If you are comparing condos from Canada, start with the dedicated Miami real estate for Canadian investors page or explore Canadian snowbirds realty. And if you already have a building in mind, contact Miami P&B Investments before your financing timeline gets tight.

The right condo can still be an excellent South Florida investment. The key is knowing what the building is telling you before you buy.