Miami rental cash flow can look simple from a distance.

You see a beautiful condo, estimate the rent, subtract the mortgage, and assume the property will carry itself.

But in Miami and South Florida, the real numbers often live below the surface.

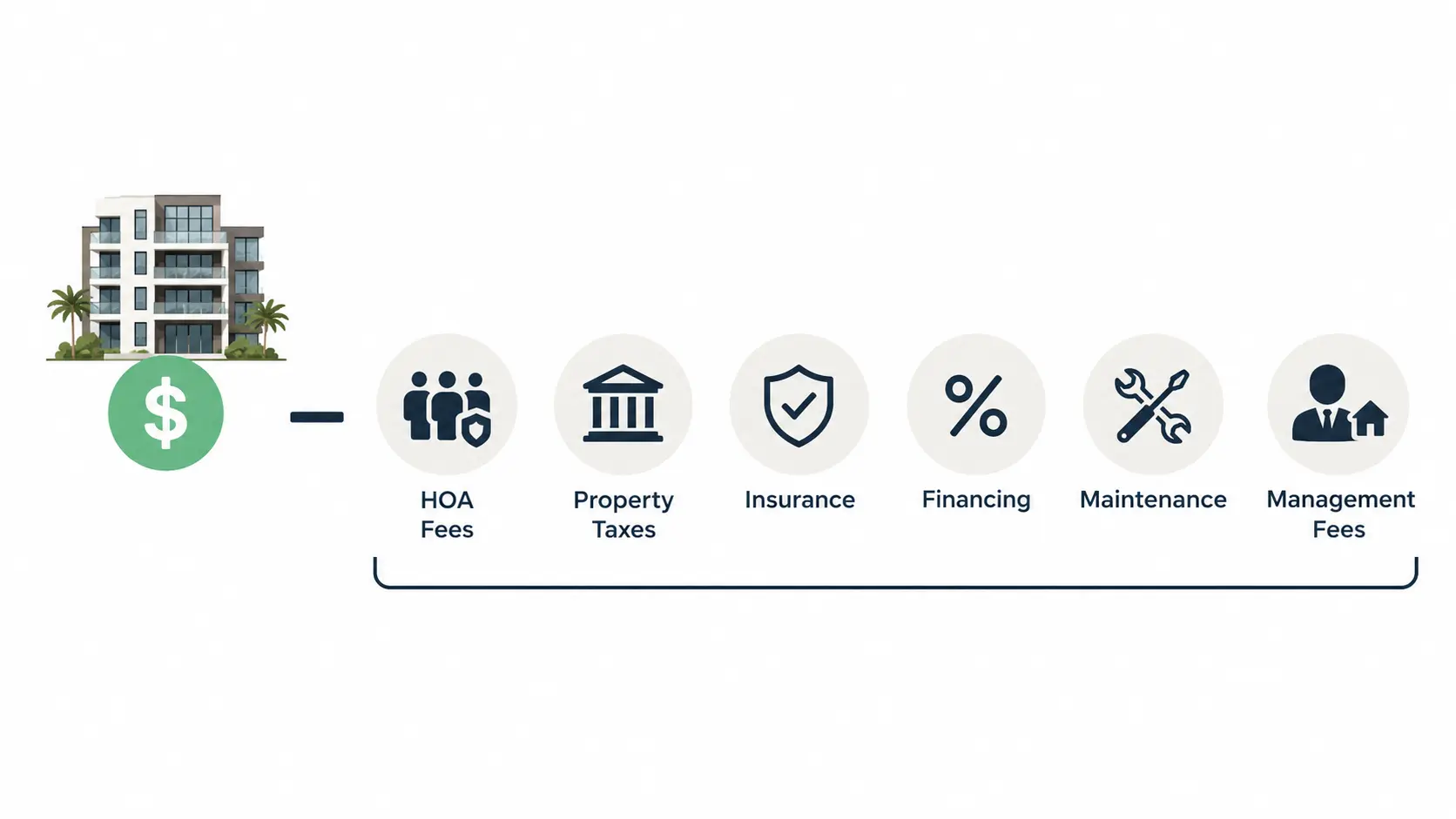

HOA fees, insurance, property taxes, rental restrictions, furnishing costs, maintenance, currency exchange, vacancy, and management can all change the outcome. A property that looks profitable in a listing spreadsheet can become tight once the full ownership picture is reviewed.

That does not mean buyers should avoid Miami. It means they should underwrite more carefully.

For Canadian buyers, snowbirds, and investors comparing Miami with other South Florida markets, understanding Miami rental cash flow is one of the smartest steps before making an offer. The goal is not just to buy a beautiful property. The goal is to buy a property that fits your lifestyle, risk tolerance, and long-term plan.

If you are still early in your search, start with Miami P&B Investments’ guide for Canadian investors buying in Miami and South Florida. Then use this article to understand the rental-income side of the decision.

What Miami Rental Cash Flow Really Means

Miami rental cash flow is the money left after rental income pays the realistic costs of ownership.

That includes the obvious costs, like mortgage payments and HOA fees. It also includes the costs buyers sometimes forget, such as vacancy, repairs, management, cleaning, utilities, accounting, licensing, reserves, and exchange-rate movement if your money starts in Canadian dollars.

A simple way to think about it is:

Monthly rental income minus monthly ownership and operating costs equals monthly cash flow.

Positive cash flow means the property produces extra income after expenses.

Break-even cash flow means the rent covers the property, but does not leave much margin.

Negative cash flow means the owner contributes money each month while hoping for appreciation, personal use, tax benefits, or future rent growth.

None of these outcomes is automatically good or bad. A waterfront condo in Brickell may have different goals than a long-term rental in Aventura or a boutique property near Coconut Grove. The key is knowing the real numbers before you buy.

Why Miami Rental Cash Flow Matters More in 2026

Miami rental cash flow matters more now because buyers are dealing with a more detailed ownership environment.

Insurance costs need to be reviewed earlier. Condo associations are under more pressure to maintain reserves and complete building requirements. Financing may be more selective. Rent rules vary sharply by city, building, and association. Property taxes can change after a sale.

For Canadian buyers, the currency layer adds another variable. Rent may come in as U.S. dollars, but part of your planning may still happen in Canadian dollars. If the exchange rate moves against you, your down payment, carrying costs, or returns can feel very different.

This is why buyers should not rely only on projected rent from a listing. A good Miami rental cash flow review looks at the full deal.

It asks:

Can the property legally be rented the way you intend?

Will the HOA allow your rental plan?

Are taxes estimated after purchase, not based only on the seller’s old bill?

Is the insurance quote realistic?

Are you budgeting enough for maintenance and vacancies?

Will the property still make sense if rent is slightly lower or expenses are slightly higher?

These are practical questions, not pessimistic ones. They help you buy with confidence.

The 9 Checks That Shape Miami Rental Cash Flow

Below are the nine checks every buyer should review before trusting a rental projection.

| Cash Flow Check | Why It Matters | What to Review |

|---|---|---|

| Rent potential | Sets the income ceiling | Comparable rents, seasonality, lease type |

| HOA fees | Can be one of the largest condo costs | Monthly dues, reserves, increases, amenities |

| Property taxes | Often reset after purchase | Estimated post-sale taxes |

| Insurance | Can change the full carrying cost | Wind, flood, building coverage, contents |

| Rental rules | Can make or break the strategy | Minimum lease term, lease frequency, waiting periods |

| Financing | Affects monthly cost and flexibility | Rate, down payment, reserves, loan type |

| Vacancy | Protects against over-optimistic projections | Seasonal gaps and tenant turnover |

| Maintenance | Keeps the property rentable | Repairs, furniture, appliances, inspections |

| Management | Critical for remote owners | Leasing, rent collection, tenant support, reporting |

1. Start With Realistic Rent, Not Best-Case Rent

The first Miami rental cash flow mistake is using the highest possible rent as the base case.

A listing may show an attractive projected rent, but you need to know how that number was calculated. Is it based on annual leasing? Seasonal rental demand? Short-term rental performance? A furnished unit? A premium view? A past tenant who paid above market?

A better approach is to build three rent scenarios.

The conservative scenario shows what the property might earn if the market softens or the unit sits vacant longer than expected.

The realistic scenario uses comparable rentals in the same building or immediate area.

The optimistic scenario shows what may be possible if timing, furnishings, view, and marketing all work well.

For example, two condos in Edgewater Miami may be in the same tower, but they may not produce the same rent. A high-floor bay-view unit with updated furniture can perform differently from a lower-floor unit facing another building.

A good Miami rental cash flow review looks at the unit, the building, the rules, and the tenant profile together.

2. Review HOA Fees Like an Investor

HOA fees are not just a monthly line item. They are part of the investment structure.

In Miami condos, HOA fees may include amenities, building insurance, security, reserves, cable, internet, water, valet, maintenance, or other services. In luxury towers, they can be high, but they may also support the lifestyle that attracts tenants and future buyers.

The question is not simply, “Is the HOA fee expensive?”

The better question is, “Does the HOA fee support the rent, resale value, and building quality?”

A high HOA fee in a well-managed building may be acceptable if the building has strong amenities, healthy reserves, reliable maintenance, and tenant demand. A lower HOA fee may look better on paper but could be risky if reserves are weak or special assessments are likely.

Before buying, review the building’s budget, financials, reserves, insurance, board minutes, and pending repairs. Miami P&B Investments’ article on Miami HOA fees is a helpful next read if you are comparing condo buildings.

HOA fees can make or break Miami rental cash flow, especially for Canadian buyers who want a lock-and-leave property.

3. Estimate Property Taxes After the Sale

Property taxes are another area where buyers often underestimate costs.

The seller’s current tax bill may not reflect what you will pay after buying. Assessed values, exemptions, millage rates, and purchase price can all affect future tax estimates.

Before relying on the seller’s tax number, use official tools such as the Miami-Dade property search and the Miami-Dade tax estimator. These tools can help you understand the property’s current assessment and build a more realistic estimate.

This is especially important for non-residents and Canadian buyers. You may not qualify for the same exemptions as a Florida primary resident. That can affect your annual carrying cost.

For a deeper overview, read Miami P&B Investments’ guide to Florida property taxes for non residents.

A strong Miami rental cash flow analysis should always include post-purchase tax planning, not just current-owner tax history.

4. Get Insurance Quotes Early

Insurance should never be an afterthought in South Florida.

Wind, flood, building coverage, contents coverage, loss of rent, and liability can all affect your numbers. Condo buyers also need to understand what the master policy covers versus what the individual owner must insure.

If a property is near the water, in a high-rise, older, newly renovated, or located in a flood-sensitive area, get quotes early. You should also review flood exposure through the FEMA Flood Map Service Center and compare that with building-specific information.

Does every Miami property have a major insurance problem?

No.

But insurance is part of due diligence. It should be reviewed before your inspection period ends, not after closing.

Miami P&B Investments’ guides on Miami property insurance costs and Miami flood zones can help you understand what to ask before moving forward.

Insurance is one of the biggest reasons Miami rental cash flow needs a realistic safety margin.

5. Confirm Rental Rules Before You Trust the Income

Rental rules are one of the most important parts of Miami rental cash flow.

A condo may look like a great investment until you discover the building only allows one lease per year, requires a long waiting period, restricts corporate ownership, limits short-term rentals, or requires board approval for tenants.

This is where buyers need to separate three layers:

City rules.

County rules.

Building rules.

Even if a city allows a certain rental use, the condo association may not. Even if a listing says “investor friendly,” the actual documents may tell a more complicated story.

Ask for the declaration, bylaws, rules and regulations, lease application, rental amendments, board minutes, and current leasing policy. You can also review broader Florida condominium resources through the Florida DBPR condominium information site.

For a deeper building-level review, read Miami P&B Investments’ article on Miami condo rental restrictions.

If the rental rules do not match your plan, the Miami rental cash flow projection is not reliable.

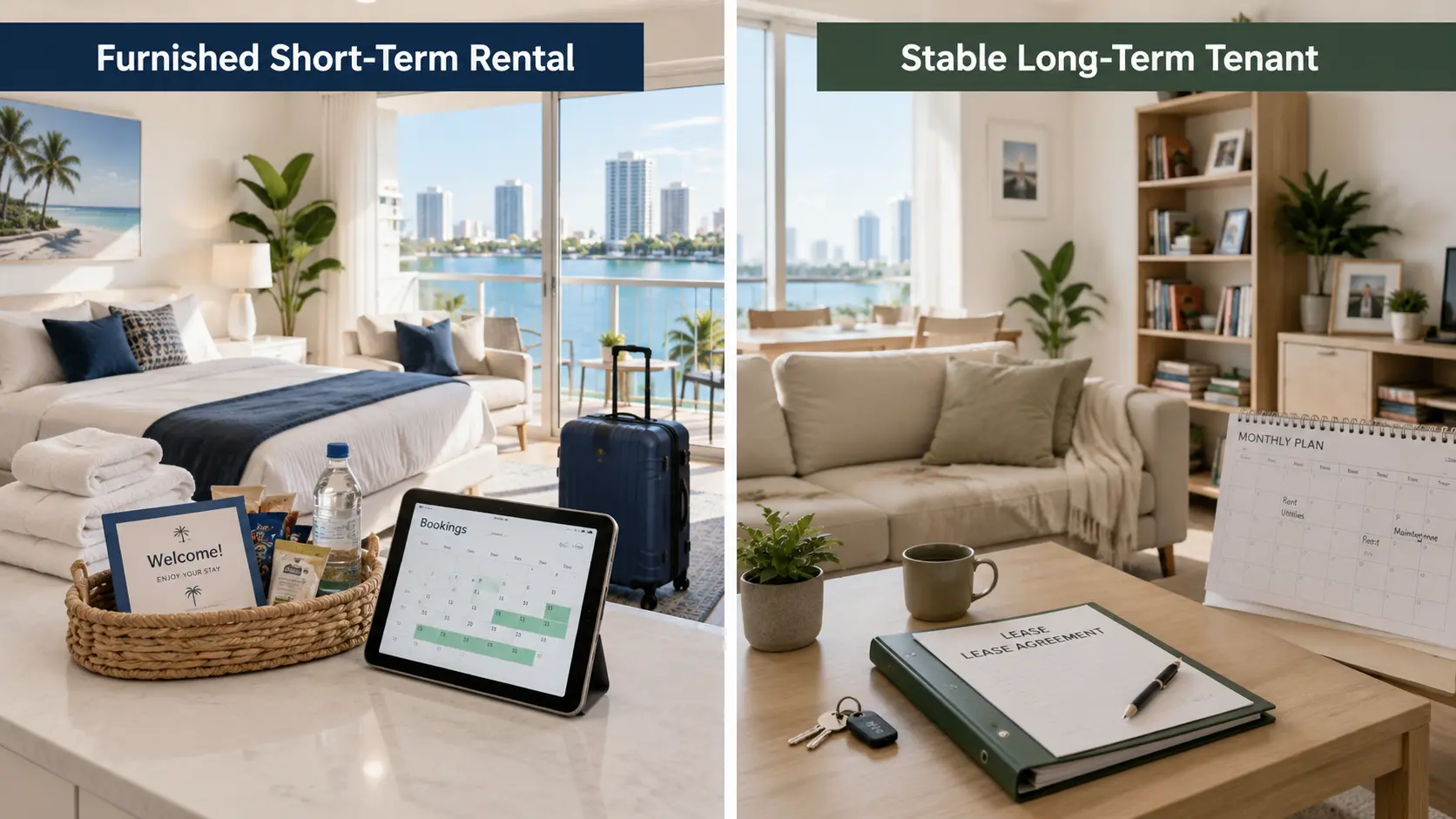

6. Compare Short-Term and Long-Term Rental Cash Flow

Short-term rentals can produce higher gross income in some Miami areas, but they also come with more moving parts.

You may need furniture, utilities, Wi-Fi, cleaning, supplies, licensing review, platform fees, guest communication, higher wear and tear, and more active management. Vacancy can also be more seasonal.

Long-term rentals may produce lower gross rent, but they can offer steadier income, fewer turnovers, and simpler management.

Which one is better for Miami rental cash flow?

It depends on the property, building rules, location, your personal-use goals, and your appetite for operational complexity.

A snowbird who wants to use the property every winter may need a flexible rental setup. An investor who wants predictable income may prefer an annual tenant. A buyer focused on luxury lifestyle may accept break-even cash flow if the property also serves as a second home.

This is why rental strategy should be decided before the offer, not after closing.

If you want hands-off rental ownership from Canada, explore Miami P&B Investments’ property management services early in the process.

7. Build a Vacancy and Maintenance Reserve

No rental property is occupied every single day forever.

Tenants move. Appliances break. Air conditioning systems need service. Furniture wears down. Paint gets marked. A special cleaning may be needed between tenants. A small leak can become urgent if nobody local is watching the property.

This is why Miami rental cash flow should include reserves.

A simple reserve can protect you from turning a good property into a stressful one. For condos, reserve planning may include unit-level repairs plus possible building-level costs. For single-family homes or townhomes, it may include landscaping, pool care, roof maintenance, pest control, and HVAC service.

Remote owners should be especially careful here. If you live in Toronto, Montreal, Vancouver, Calgary, or elsewhere in Canada, you need someone local who can respond quickly.

Miami P&B Investments offers property maintenance services for owners who want a local team watching the details.

The strongest Miami rental cash flow plans always include money for the unexpected.

8. Account for Financing and Currency Movement

Financing changes the monthly picture.

A cash buyer may focus on net yield after expenses. A financed buyer must also account for principal, interest, lender reserves, insurance escrow, tax escrow, and loan terms. Canadian buyers may also face foreign-national lending requirements, larger down payments, and extra documentation.

If your down payment starts in Canadian dollars, currency timing matters too. A small exchange-rate move can affect your real purchase cost, closing funds, and return calculation.

This does not mean Canadians should avoid Miami. It means the numbers should be built in both U.S. dollars and Canadian-dollar equivalents where relevant.

Miami P&B Investments’ guides on U.S. mortgages for Canadians in Florida and currency exchange risk when buying in Miami are useful resources before finalizing your strategy.

Financing and currency planning can turn a basic Miami rental cash flow estimate into a much clearer investment decision.

9. Review Exit Value, Not Just Monthly Income

Cash flow matters, but it is not the only measure of a property.

A unit with slightly lower monthly cash flow may still be attractive if it has strong resale demand, excellent location, better building quality, and long-term appreciation potential. Another unit may show better short-term income but carry more risk because of weak building financials, limited financing options, or difficult rental rules.

Ask yourself:

Who will buy this property from me later?

Will future buyers be able to finance it?

Will the building still look competitive in five or ten years?

Are HOA fees likely to remain manageable?

Is the neighborhood improving, stable, or becoming oversupplied?

Areas like Miami, Brickell, Edgewater, Coconut Grove, Aventura, Wynwood, Bay Harbor Islands, Fort Lauderdale, Boca Raton, and West Palm Beach can all serve different buyer profiles. The best choice depends on your goals.

A smart Miami rental cash flow review includes both income today and resale strength tomorrow.

A Simple Example of Miami Rental Cash Flow

Imagine two Miami condos with similar purchase prices.

Unit A has higher projected rent but also higher HOA fees, stricter rental rules, older systems, and uncertain insurance costs.

Unit B has slightly lower rent but clearer rental rules, stronger building reserves, lower vacancy risk, and better management history.

At first glance, Unit A may look better.

After due diligence, Unit B may produce more reliable Miami rental cash flow because fewer things can go wrong.

This is why buyers should avoid choosing based only on the rent number. The better question is: which property gives you the cleanest net result after realistic expenses?

What Canadian Buyers Should Watch Closely

Canadian buyers often approach Miami with a hybrid goal.

They may want rental income, personal winter use, long-term appreciation, and a future retirement option. That is a different strategy from a purely local investor looking only at monthly net income.

For Canadians, the most important Miami rental cash flow questions are:

Can I rent the property when I am not using it?

Will the building allow my preferred rental pattern?

Can the property be managed without me flying to Florida?

Are taxes, FIRPTA, and cross-border reporting being reviewed properly?

Is the income strong enough after USD expenses and CAD exchange-rate considerations?

Should I buy personally, through an entity, or with another structure after professional advice?

Miami P&B Investments’ Canadian Snowbirds Realty page is a useful starting point for seasonal buyers who want both lifestyle and investment value.

When Negative Cash Flow May Still Make Sense

A negative monthly number does not always mean a bad purchase.

Some buyers accept modest negative cash flow because they plan to use the property personally, hold long term, benefit from appreciation, or eventually convert it to a different use. A luxury second home may not be judged the same way as a pure rental investment.

However, negative cash flow should be intentional.

It should not happen because taxes were underestimated, insurance was ignored, rental rules were misunderstood, or the HOA budget was not reviewed.

The right question is not, “Must every Miami property cash flow immediately?”

The better question is, “Does this property’s full financial picture match my plan?”

That is the difference between strategic ownership and surprise ownership.

How Miami P&B Investments Helps Buyers Review the Numbers

Miami rental cash flow is not just about rent. It is about buying the right property, in the right building, with the right rules, realistic expenses, and a management plan that works after closing.

Miami P&B Investments helps Canadian, U.S., and international buyers compare properties across Miami and South Florida with a practical ownership lens. Through real estate services, property management, accounting support, legal coordination, construction guidance, and ongoing maintenance, the team helps buyers look beyond the listing photos and understand the real ownership experience.

If you are comparing condos, vacation homes, or rental properties in Miami, start with a clear cash-flow review before you make an offer.

A beautiful property is exciting.

A beautiful property with a realistic plan is stronger.

To discuss your goals, rental expectations, and ownership structure, contact Miami P&B Investments and build your Miami rental cash flow plan before you buy.